By Pam Martens and Russ Martens: Might 22, 2023 ~

Basically whatever the typical American has actually checked out the banking crisis is incorrect. And there is at least a prima facie case that might be made that Huge Media is accountable for that false information.

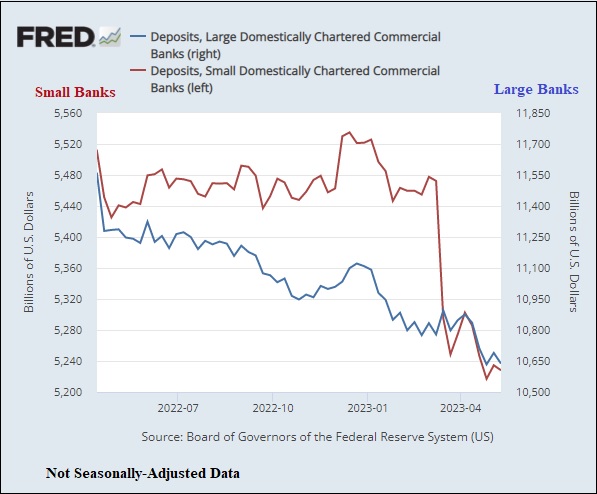

Let’s begin with the lots of mainstream media reports that little banks were bleeding deposits and these deposits were flooding into the most significant banks in the U.S. as a safe house. Those reports provided the unique impression that the mega rely on Wall Street are seen by Americans as a safe location to stow away cash, never ever mind that they exploded the U.S. monetary system in 2008 and still have more than $200 trillion in derivatives prowling in the shadows.

According to FRED information assembled by the St. Louis Fed (see chart above), bank deposits at the 25 biggest U.S.-chartered business banks peaked at $11.556 trillion on April 13, 2022, then entered into a consistent drop that eliminated $457 billion of deposits by December 12, 2022. On the other hand, the more than 4,000 little U.S. banks, on the other hand, produced a $25 billion gain in deposits in the very same time period.

It was not up until all of those news short articles appeared in March and April of this year, stating that little banks were losing deposits, that the little banks really saw a sharp drop in their deposits.

On March 13 of this year, the Financial Times ran this heading: “ Big United States banks swamped with brand-new depositors as smaller sized lending institutions deal with chaos” The subhead was much more doubtful, reading: “Failure of Silicon Valley Bank triggers flight to similarity JPMorgan and Citi.” (JPMorgan Chase has actually been charged with an extraordinary 5 felony counts by the U.S. Department of Justice over the previous 9 years. See JPMorgan’s Board Made Jamie Dimon a Billionaire as the Bank Rigged Markets, Washed Cash, and Confessed to 5 Felony Counts) Citigroup’s stock has actually been a basket case considering that the monetary collapse in 2008 Citi did a 1-for-10 reverse stock split in 2011 to window gown its stock rate.

On April 28, the Bloomberg writer, John Authers, composed a column that was syndicated to the Washington Post. Authers included this deceptive details about the 4 biggest U.S. banks: JPMorgan Chase, Bank of America, Wells Fargo and Citigroup’s Citibank.

” This summary from the Canadian company Palos Management discusses nicely why the larger banks are still okay:

” The very first quarter’s efficiency of the huge 4 followed a broad agreement that the huge banks have actually taken advantage of enormous depositor inflows, plainly associated to the well-documented liquidity tensions facing their smaller sized, regionally based brethren. This need to come as not a surprise. The panic-fueled depositor exodus from the smaller sized banks to the bigger ‘too huge to stop working’ banks is just a logical choice. Defense of capital guidelines.”

As we reported on Might 8, the real truth is this: Deposits at JPMorgan Chase, Bank of America and Wells Fargo Shrank by $465 Billion Y-O-Y; More than Two times the Overall of 4,000 Little Banks Because short article, we offered granular information as follows:

” The deposit losses at JPMorgan Chase, Bank of America and Wells Fargo are more than two times what the 4,000 little banks lost in overall throughout the very same duration. Their combined loss in deposits was simply $210 billion …

” Bank of America and Wells Fargo not just lost those big deposit amounts on a year-over-year basis, however both banks saw deposits fall throughout the previous 5 quarters, consisting of the quarter ending March 31, 2023 when headings were stating that they were seeing huge inflows of deposits as an outcome of the banking crisis. JPMorgan Chase lost deposits in each of the quarters in 2022 and after that saw a little boost in deposits in the very first quarter of this year– most likely from all of those deceptive headings. (This details is quickly gotten from the monetary declarations the companies submit openly with the SEC.)”

Over this previous weekend, the Wall Street Journal ran a huge short article on how the banking crisis has “ just made JPMorgan more powerful” ( Paywall) Press reporter David Benoit composes as follows about JPMorgan Chase’s purchase of the collapsed bank, First Republic:

” Yet JPMorgan’s program of strength, for numerous, exposed a weak point in the U.S. monetary system. The bank and its biggest competitors have actually ended up being so huge, their reach so comprehensive, that the federal government would nearly certainly action in to avoid their failure. That implicit warranty motivates individuals and organizations to move their cash to them in times of tension producing a feedback loop that makes huge banks larger at the expenditure of their smaller sized peers.”

The only feedback loop we’re seeing is the echo chamber of the mainstream company press.

What is not in disagreement about JPMorgan Chase’s grab of First Republic Bank is the following: JPMorgan Chase was initially called First Republic’s “rescuer” by the media. Then JPMorgan Chase ended up being Very first Republic’s “consultant” to discover tactical choices for its survival. Then JPMorgan Chase put a minimum of 800 of its staff members to deal with doing due diligence in order to purchase First Republic for itself and get a sweetie offer from the FDIC. The sweetie regards to the offer consist of the FDIC consuming 80 percent of any losses on single-family domestic home mortgages for 7 years and 80 percent of any losses on business loans, consisting of business realty, for 5 years. The FDIC likewise, bizarrely, handed JPMorgan Chase a $50 billion, five-year fixed-rate loan at a concealed rates of interest.

All of this raises the concern, who got the bailout: uninsured depositors initially Republic Bank or JPMorgan Chase?